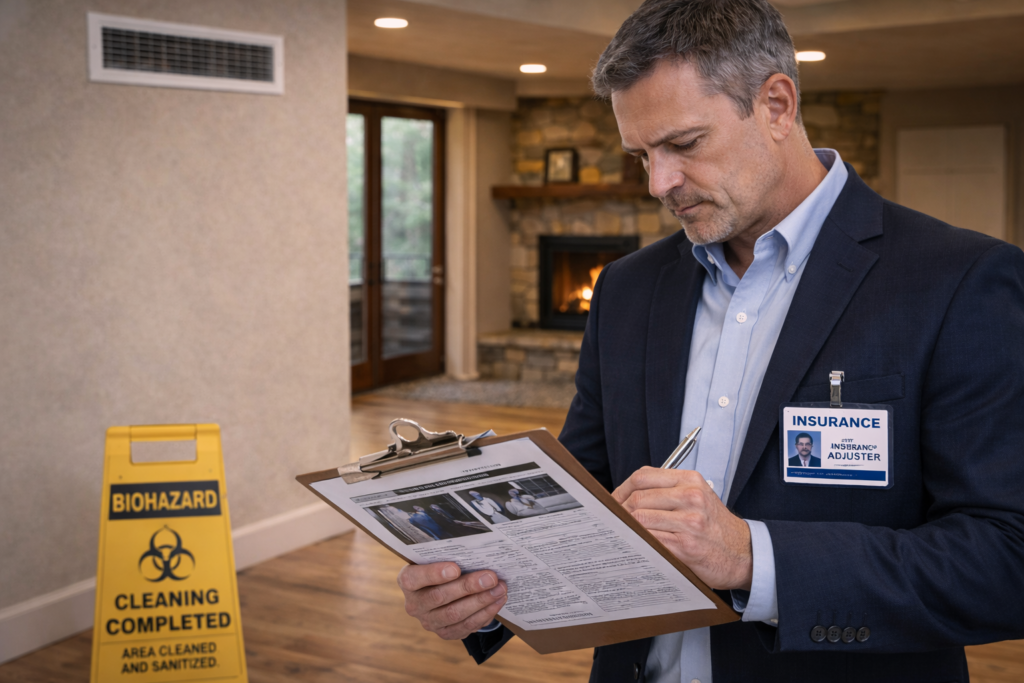

What Do Insurance Companies Look for in Biohazard Remediation Documentation?

Insurance companies evaluate biohazard remediation based on documentation quality, process completeness, and defensibility—not appearance alone. Clear records of source removal, HVAC remediation, verification steps, and compliance alignment determine claim outcomes and liability protection.

Introduction: Clean Isn’t the Question—Proof Is

From an insurance perspective, a biohazard claim isn’t resolved when a space looks clean. It’s resolved when the cleanup can be defended on paper.

Adjusters don’t inspect every duct. Compliance officers don’t smell every room. Facility decision-makers don’t want reassurance—they want documentation that survives scrutiny.

The question insurers are asking is simple and unforgiving:

If this claim is challenged six months from now, can we prove the remediation was complete, reasonable, and compliant?

That’s where most cleanups quietly fail.

The Insurance Lens: Process Over Perception

Insurance carriers evaluate biohazard remediation through three primary filters:

- Was the contamination source identified and removed?

- Were secondary exposure pathways addressed?

- Is there documentation to support both?

Visual cleanliness is irrelevant without process evidence. A pristine room with weak documentation is a liability. A well-documented remediation with methodical steps is defensible—even if it cost more upfront.

Documentation Elements Insurers Expect to See

While requirements vary by carrier and claim type, strong remediation files consistently include:

- Incident scope and contamination classification

- Source removal methodology

- Area containment strategy

- HVAC inspection and remediation notes

- Cleaning and disinfection protocols used

- Waste handling and disposal records

- Odor control or neutralization steps

- Post-remediation verification (including air testing when appropriate)

- Photographic and time-stamped records

Missing one element doesn’t always kill a claim. Missing several creates friction, delays, or denials.

HVAC Remediation: A Silent Documentation Gap

As shown in Articles #12 and #13, HVAC systems are frequent contamination reservoirs—and frequent documentation failures.

Insurers increasingly ask:

- Was the HVAC system evaluated for contamination?

- Were ducts, coils, or air handlers cleaned if exposed?

- Was the system operated before clearance testing?

- Is there proof the air system won’t re-distribute contaminants?

When HVAC documentation is absent, claims become vulnerable—even if air tests passed.

Also Read ☣️Does Your HVAC System Spread Contaminants After a Biohazard Event?

Why Air Testing Alone Doesn’t Satisfy Adjusters

Air testing is useful, but insurers understand its limits. A single passing test does not confirm:

- Removal of embedded contamination

- Long-term occupant safety

- Prevention of re-aerosolization

Adjusters view air tests as supporting evidence, not final proof. Without context—what was cleaned, when systems were reactivated, what materials remained—test results float without meaning.

Compliance Officers Care About “Reasonableness”

Most remediation standards are guidance-based, not prescriptive. This means compliance isn’t about perfection—it’s about reasonable, defensible decision-making.

Good documentation answers:

- Why certain steps were taken

- Why others were not

- How decisions aligned with risk level

This protects facilities from regulatory criticism and post-occupancy complaints.

Facility Decision-Makers: Where Conversion Pressure Lives

Facility leaders don’t want to micromanage remediation. They want outcomes:

- No repeat incidents

- No employee complaints

- No surprise liability

- No insurance disputes

The fastest way to deliver that is not speed—it’s documentation clarity. Providers who explain, record, and verify their process reduce long-term risk and build trust where it matters most.

What Strong Documentation Actually Buys You

For insurers, compliance teams, and facilities alike, strong remediation records provide:

- Faster claim resolution

- Reduced dispute risk

- Clear audit trails

- Protection against re-exposure claims

- Confidence in re-occupancy decisions

Documentation isn’t paperwork. It’s risk insulation.

The Bottom Line: Remediation That Can’t Be Proven Didn’t Happen

In biohazard cleanup, the work only counts if it can be demonstrated after the fact. Insurance companies don’t pay for effort—they pay for verifiable process.

Clean spaces fade from memory. Documentation endures.

And when questions arise months or years later, it’s the file—not the floor—that determines who carries the risk.

Also Read ☣️Does Your HVAC System Spread Contaminants After a Biohazard Event?

FAQs

1. What documentation do insurance companies require after biohazard cleanup?

They typically require proof of source removal, cleaning methods, HVAC evaluation, verification steps, and proper disposal records.

2. Is photographic documentation important for biohazard claims?

Yes. Photos provide time-stamped evidence of conditions, progress, and completion.

3. Do insurers expect HVAC systems to be addressed?

Increasingly yes, especially if air movement could spread contamination.

4. Are air quality tests enough for insurance approval?

No. Tests support documentation but do not replace process records.

5. What causes delays in biohazard insurance claims?

Incomplete documentation, unclear scope, and missing remediation steps.

6. Do compliance officers review remediation files?

Yes, particularly in regulated environments like healthcare or education.

7. How long should remediation records be retained?

Often several years, depending on industry and risk exposure.

8. Can poor documentation increase liability later?

Yes. It weakens defense against re-exposure or negligence claims.

9. Is cost transparency important in documentation?

Yes. Clear line-item justification supports claim approval.

10. What defines a defensible biohazard remediation?

Clear scope, complete process, HVAC consideration, and verifiable records.